Abstract

The 2026 Iran-Israel-US war has severely disrupted global supply chains, primarily through near-halt of traffic in the Strait of Hormuz — which normally carries 20% of seaborne oil and 20-25% of LNG — along with escalated threats in the Red Sea and damage to energy infrastructure. This has caused sharp surges in oil and LNG prices, higher freight rates, rerouting via the Cape of Good Hope (adding 10–14 days), and shortages in fertilizers, aluminum, helium, and petrochemicals, threatening agriculture, manufacturing, and consumer goods worldwide.South Asia, heavily reliant on Middle Eastern energy and fertilizers, faces rising costs, shipping delays, and risks to food security and exports. As of early April 2026, countries like Bangladesh, India, and Pakistan are mitigating impacts through emergency imports (including from Russia with waivers), fuel rationing, conservation measures, supplier diversification, and strategic reserves. Navigating Supply Chain Disruptions in 2026, while these steps have prevented immediate collapse, they bring higher inflation and economic strain, especially for Bangladesh’s RMG sector.

Keywords: Navigating Supply Chain Disruptions in 2026

Introduction

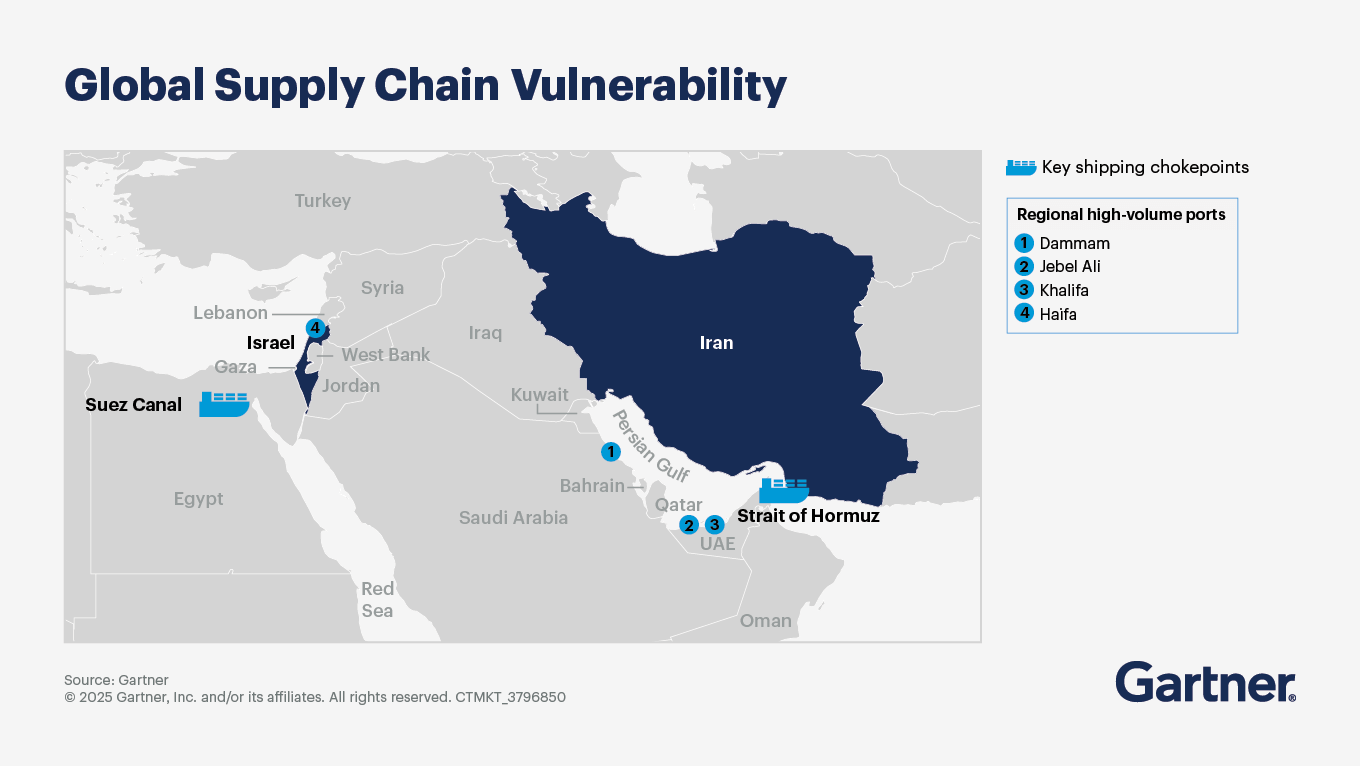

Navigating supply chain disruptions in 2026 US-Israel-Iran war that began with joint US-Israeli strikes on Iranian targets on February 28, 2026 are significant and wide-ranging. They primarily stem from Iran’s retaliation, including the near-total effective closure or severe restriction of the Strait of Hormuz,a critical chokepoint for energy and commodities, attacks on regional infrastructure, and renewed threats/activities by Iran-backed Houthis in the Bab el-Mandeb Strait i.e.,Red Sea entrance. This creates a dual chokepoint crisis affecting maritime trade.

Main Causes of Strait of Hormuz disruptions

Normally handles 20% of global seaborne oil i.e,20 million barrels/day and ~20-25% of LNG. Navigating Supply Chain Disruptions in 2026, we see that traffic has dropped dramatically to a trickle or near-halt in places, with attacks on ships, threats to vessels, and force majeure declarations by exporters. Some limited passages have resumed under high risk, but full normalization is uncertain.

Red Sea , Bab el-Mandeb threats

Houthis have escalated or threatened actions in support of Iran, compounding earlier disruptions. This forces additional rerouting around Africa’s Cape of Good Hope for many routes adding 10–14+ days and thousands of nautical miles.

Infrastructure damage and airspace issues

Strikes have hit energy facilities e.g., in Qatar, ports, and logistics hubs, disrupting air cargo and regional shipping. Key Impacts on Supply ChainsEnergy (Oil and LNG). Sharp oil price surges at times approaching or exceeding $100–120/barrel before some moderation. Higher fuel costs raise transportation, manufacturing, and consumer prices worldwide. LNG exports from Qatar ,a major global supplier, severely disrupted, with force majeure on contracts and potential multi-year recovery for damaged facilities. This affects power generation, heating, and petrochemical feedstocks in Asia and Europe.

Raw Materials and Commodities

For fertilizers, middle-east is a key producer/exporter; disruptions threaten spring planting seasons, potentially reducing crop yields and raising food prices especially in import-dependent regions like South Asia, Africa, and parts of Latin America. Global fertilizer prices have risen sharply.

Aluminum

Gulf producers (8% of global supply) have halted shipments or rerouted, driving up prices and affecting automotive, construction, packaging, electronics, and aerospace.

Helium and others

Sourced from Qatar’s natural gas processing; shortages impact semiconductors, medical imaging (MRI), and high-tech manufacturing. Petrochemicals/plastics for packaging, clothing, consumer goods, sulfur fertilizer/nickel processing, and naphtha petrochemical feedstock.

Shipping and Logistics

Container and tanker freight rates rising with surcharges, war-risk premiums, and longer routes. Capacity strained; some lines suspended services or added fees i.e.,$2,000–$4,000+ per container in some cases. Air cargo hit hard as delays for perishables, electronics, pharmaceuticals, and parts due to airspace restrictions and rerouting. Port congestion and inventory shortages emerging as vessels are stranded or delayed.

Manufacturing and Consumer Goods

Higher energy and input costs ripple into electronics, pharmaceuticals ingredients i.e., from Asia, automotive parts, construction materials such as steel, cement, aluminum, textiles/garments, and plastics. Potential shortages or price hikes for everyday items, with greater effects on import-heavy economies. Construction and food sectors are particularly exposed.

Broader and Regional Effects

Inflation and economic pressure is rising. Transport, energy, and material costs contribute to higher consumer prices globally. Developing regions face heightened food security risks. Short disruptions cause immediate price spikes and delays; prolonged ones (weeks to months) could lead to deeper shortages. Recovery may take 1–2 months or longer even after routes reopen, due to backlogs and damaged infrastructure. Some alternative suppliers (e.g., US LNG in certain scenarios) or rerouting beneficiaries may gain, but it’s a net negative with high uncertainty.

Response from businesses

Businesses are responding by rerouting shipments, building inventory buffers, seeking alternative suppliers, and passing on surcharges. Navigating Supply Chain Disruptions in 2026, governments have released strategic reserves in some cases to ease energy pressure. The situation remains fluid as of early April 2026, with ongoing military actions, diplomatic efforts, and market volatility. Impacts vary by industry and region—Asia (heavy oil/LNG importer) and Europe face strong effects, while the US is somewhat more insulated but still sees higher costs.

Supply disruption in South Asia

Bangladesh and other South Asian countries (India, Pakistan, Sri Lanka) are not fully “evading” the supply chain disruptions from the 2026 US-Israel-Iran war and the effective closure/restriction of the Strait of Hormuz (and related Red Sea issues). These nations are heavily dependent on Middle Eastern oil, LNG, and fertilizers, so the disruptions have caused higher energy prices, shipping delays, stranded cargo, and risks to agriculture and exports. However, they are actively mitigating the impacts through a mix of short-term conservation,rationing, emergency imports, diversification of suppliers, and government interventions.

Till today South Asia situation

As of early April 2026 (roughly one month into the crisis), these measures have prevented immediate collapse but come with higher costs, inflation risks, and strain on economies—especially for fuel-dependent industries like Bangladesh’s ready-made garments (RMG) sector. Navigating Supply Chain Disruptions in 2026,

Bangladesh’s Mitigation Strategies Bangladesh is one of the most exposed due to its reliance on Gulf fuel (for power/generators) and fertilizers (for rice/agriculture), plus RMG exports facing logistics issues.Emergency shipments secured from China, India, PetroChina, and Vitol (totaling ~150,000+ metric tons in March, covering about one month’s demand). Seeking a US sanctions waiver (similar to India’s) to import up to 600,000 metric tons of Russian diesel. Exploring additional sources like the US, Uzbekistan, Kazakhstan, Angola, and Australia. Fuel rationing introduced (capped sales, troops guarding depots to prevent hoarding).

Fertilizer supplies

Canceled tenders for 200,000 tons of urea due to Hormuz uncertainty. Shifting to alternative suppliers including China, Egypt, and Russia (requesting sanctions relief for Russian imports). Some domestic fertilizer plants shut or slowed due to gas shortages.

Energy conservation and demand reduction

Universities, foreign-curriculum schools, and coaching centers moved online; rolling blackouts (up to 5 hours); reduced non-essential electricity use (e.g., during Eid). While Navigating Supply Chain Disruptions in 2026, garment factories using backup generators are at risk of shutdowns from diesel shortages.

Logistics and RMG sector

Stranded containers (over 1,000 reported early on); higher freight/insurance costs and delays. Businesses operating under uncertainty, with some factories at risk of closure and wage issues. Buyers pushing for lower prices amid rising operating costs.

Contingency actions

Supplies were estimated to last 9–14 days in some scenarios, prompting rapid contingency actions.Other South Asian CountriesIndia (least impacted due to proactive diversification):Imports energy from 41+ countries (up from 27 previously). Secured ~60 days of oil supply; majority now via non-Hormuz routes. Ramped up Russian crude purchases with US waiver; boosting imports from Africa, US, and others. Maximizing domestic LPG production and diverting gas to priority sectors (power, industry). Releasing strategic reserves as needed.

Pakistan’s austerity measures

25% government salary cuts, travel bans, limits on wedding guests, fuel allocation reductions (50% cuts to departments, non-essential vehicles off roads). Four-day work week + 50% work-from-home for government; schools/colleges closed or shifted online (2 weeks). Fuel prices up ~20% with queues at stations. LNG supplies to fertilizer sector suspended. Solar energy expansion (post-2022) provides a partial buffer for electricity.

Sri Lanka still recovering from 2022 crisis

Four-day work week (Wednesdays off for public institutions, schools, non-essential workers). Fuel price hikes (8–25%). Reintroduced QR-code National Fuel Pass with strict weekly quotas/rationing to prevent hoarding. Seeking oil supply assurances and support from India via Indian Oil Corporation.

Common Regional Approaches Conservation and rationing

Reduced workweeks, remote work, school closures, fuel caps, and behavioral appeals to cut non-essential use. Heavy pivot to Russia (with waivers), plus Africa, US, Australia, China, Egypt for fuel/fertilizers/LNG. Drawing down stocks, diplomatic efforts for safe passage or alternative routing. Calls for more domestic production, renewables (e.g., Pakistan’s solar), and reduced dependence on single chokepoints.

Conclusion

Prolonged disruption could worsen fertilizer shortages, raise inflation, and hit RMG/agriculture hard in Bangladesh. Impacts are uneven—India is better buffered, while Bangladesh, Pakistan, and Sri Lanka face tighter constraints. The situation is fluid; these are mostly short-term fixes while hoping for diplomatic resolution or reopened routes.

Further Reading:

1.“UN to vote on Hormuz resolution as China opposes authorization of force”. 2026.

2.Wilson, Jason (19 March 2026). “West Point analysis warns that strait of Hormuz blockade will strangle US defense in

3.https://youtu.be/R4VlzVkROC0?si=bJ3Px7bYyzM42YMr